Skip to content

Skip to content

The European automotive aftermarket is stronger than ever.

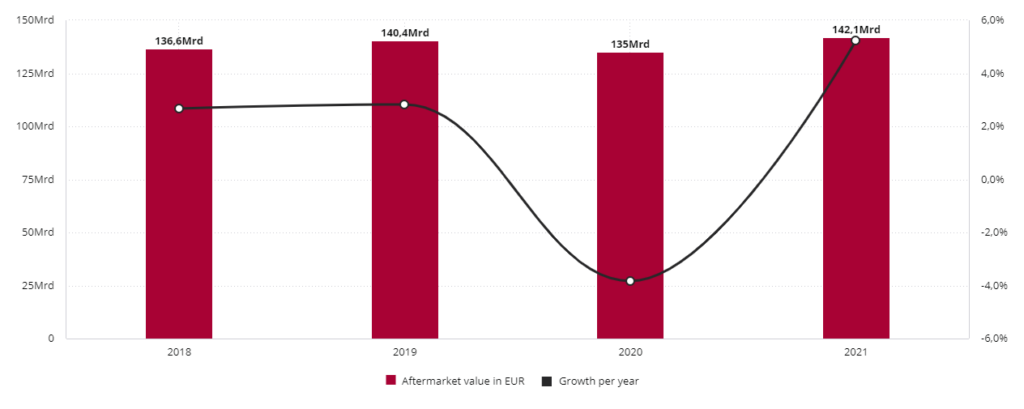

According to the recently published 10th edition of the Car Aftermarket Europe Report 2022, which contains the latest and verified data from 34 European countries, the aftermarket in Europe grew by 5% in 2021.

After a drop of 3,8% in 2020 the total value of sold spare parts in Europe has recovered and gained. Already during the pandemic, the aftermarket has shown its resilience towards larger crises, as it did in 2008. The year 2021 was full of crises as well. The pandemic situation, the shortage of supplies, the difficulties with the logistic chains etc..

Most of the circumstances have led to better performance in the Aftermarket, as the car drivers have to drive their current cars for a longer period. The situation of uncertainty has continued and even accelerated in 2022 due to the war in Ukraine, energy sourcing issues, and inflation.

Aftermarket value development in Europe between 2018 and 2021

The report provides detailed information on each country’s passenger car and truck aftermarket. The report is the ideal support to understand the big picture of every single country in Europe. It gives a good overview of the aftermarket structure including the distribution and garage structure. One of the current trends that have accelerated during the pandemic crisis is that car manufacturers are becoming more active in the independent car aftermarket channel. Disregarding this trend, the market is still divided into two major channels. Both channels are described in their structure and total value.

Further, the report contains the number of car repair stations per country with a split into the different workshop types.

Additionally, the most important players like spare parts dealers, trade and buying groups, and the different garage types are represented with a company profile. The profiles contain the address, number of outlets, membership of national and international trade groups, and annual turnover.

The Car Aftermarket country reports are up to 120 pages long and include tables and graphs reflecting the specifics of each local market.

The reports cover not only the European Union plus Norway, Switzerland, and the United Kingdom, but all countries in the East up to and including Belarus, Russia, and Turkey. This makes the reports a valuable source of information, offering a unique insight into the European automotive aftermarket.

The Car Aftermarket Europe Report 2022 is an important tool for the European automotive industry. It provides a comprehensive and accurate overview of the European aftermarket and helps companies develop their strategies and determine their position in the market.

Table of content:

- Introduction

- Summary

- General situation

- The car data

- The aftermarket situation

- The aftermarket volume

- Comparison 2020 vs. 2021

- Comparison with Germany and Europe

- General Country specific information

- General data

- Macroeconomic data

- Vehicle data

- Passenger cars data (total registrations and new registrations per year)

- Passenger car parc by brand

- Truck Fleet

- Bus fleet

- Aftermarket Structure

- OES Structure

- OES trade and buying groups

- OES garage marketing systems

- Important car dealers / car dealer groups

- Structure of IAM distribution

- Traditional IAM distribution

- Trade and buying groups

- Specialized trade and buying groups

- Wholesalers / Distributors

- Specialized distributors

- Truck parts distributors

- Auto centers

- Trade marketing systems

- Retail chains

- Direct marketers

- E-Commerce companies

- IAM repairers

- Fast fitter

- Garage marketing systems

- Garage marketing systems for mechanical repairs

- Garage marketing systems for specialised repairs

- Truck specialists

- Traditional IAM distribution

- OES Structure

- Aftermarket volume in value by 10 product groups

- Annex – Company profiles

- OES companies – profiles

- OES car trade and buying groups

- OES garage marketing systems

- Important car dealers / groups

- IAM distributors – profiles

- Trade and buying groups

- Specialised trade and buying groups

- IAM large distributors

- IAM specialised distributors

- IAM truck parts distributors

- IAM direct distributors

- IAM autocentres

- IAM trade concepts

- IAM garages – profiles

- IAM fast fit chains

- IAM garage marketing systems

The Car Aftermarket in Europe 2022

This category contains 35 different country reports, each of which provides detailed information on the automotive industry and aftermarket in a specific country. Each report is divided into several sections, with the structure and content of the report varying slightly depending on the specific country being analyzed.

Generally, the reports begin with an introduction and summary, which provide an overview of the current state of the automotive industry and aftermarket in the country. The summary may include data on the number of vehicles in the country, the state of the economy, and the size and structure of the aftermarket.

The remaining sections of the report typically provide more detailed information on various aspects of the automotive industry and aftermarket in the country. This may include information on the structure of the OEM and IAM sectors, the distribution channels for aftermarket products, the types of products and services available in the aftermarket, and the major players in the industry.

Overall, these reports offer a comprehensive overview of the automotive industry and aftermarket in each of the 35 countries covered, providing valuable insights and data for anyone interested in this sector.