Skip to content

Skip to content

Key findings

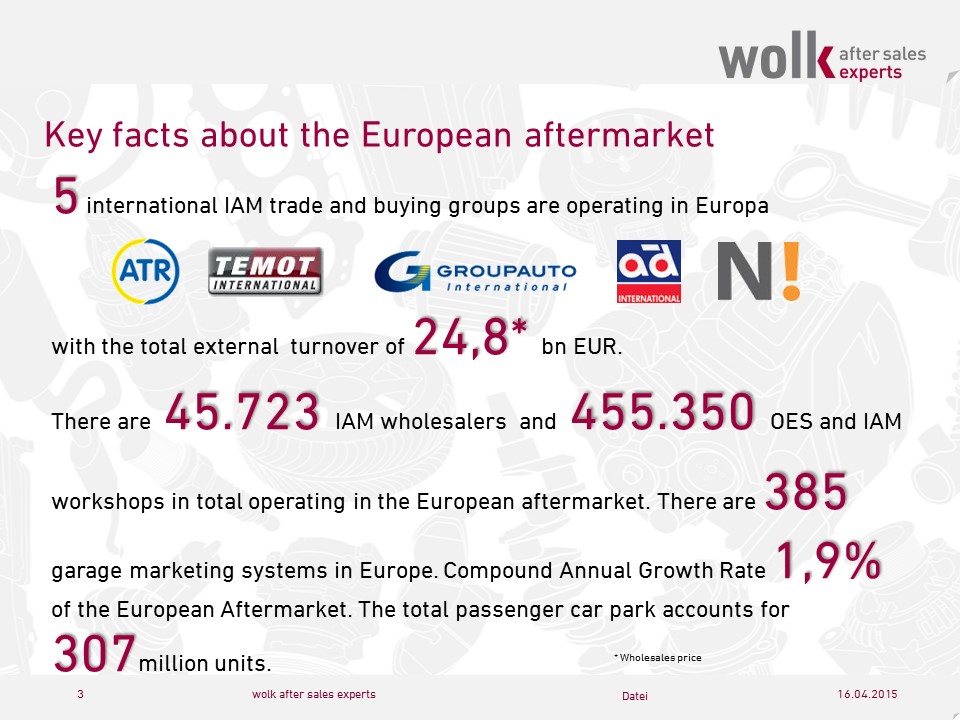

With an average annual growth rate by 1.9% in 2013, the car aftermarket is once again proving to be a stable economic factor in Europe.

Almost 18% of the European aftermarket is accounted for Germany.

The entire car after sales market in Europe, including all acquired components for a car, generated about 119 billion Euros in 2013 (based on retail prices excluding VAT, only material without salary). The components which were included in the calculation of the market volume are wear parts, body parts, engines, transmissions, electrical parts, automotive glass, chemicals, oil, tires, paint.

These are some of the key results from the new report “The Car Aftermarket in Europe 2014” created by wolk after sales experts.

The team of highly specialized aftermarket analysts from Bergisch Gladbach (Germany) has recently published the 2014 edition of the European aftermarket structure analysis for 34 European countries for the third time in a row after 2009 and 2012.

An after sales alliance network with after sales specialists in several European countries supported th preparation of this report with their local expertise.

Large differences

The European aftermarket is far from being homogeneous. This study pointed out nine different clusters of countries which have large differences in their sales and turnover behavior. A motorist in Scandinavia pays per year about 588 Euros for new car components for example. This represents an increase of nearly 3% towards 2009. Motorists in Russia and Belarus however spend only 258 Euros for the spare parts of their cars.

Constant change

After sales manager in industry, trade and craft are faced with major changes in the various European aftermarkets. To be mentioned in this context for example are the acquisitions in the car parts wholesale sector by Sator / LKQ in the Benelux countries, the mergers and acquisitions in the German market (e.g. WM bought Trost and Stahlgruber acquired majority interest in PV Automotive) or the growing importance of e-commerce in the aftermarket.

Development and changes which were out of imagination 10 years ago become reality.

Helmut Wolk, director of wolk after sales experts describes the situation in the European aftermarket as follows: ”Often you cannot avoid the impression that the market participants are exposed to a chaotic market scenario that has no fixed boundaries where concepts, priorities and schedules shift quickly.”

Data Mining and Validation

The researched data is based on detailed car park data, economic data of the investigated market partners, primary research data from expert interviews with key market players like distributors and repairers in all countries and secondary statistical data.

Finally, the material flow in the supply chain was validated by a “top down method” (material flow from wholesale to the workshop) and a “bottom up method” (material acquired from workshops).

All data is extracted from the database “After Sales ACCESS” developed by wolk after sales experts which bundles all information about the 34 European countries at one place and offers various evaluation possibilities. The car aftermarket report in Europe is an excellent example for such an evaluation via the database.

Content for each of the 34 countries in Europe

- Car park data

- Market volume by 10 product groups

- Market structures

- Traditional OES and IAM distribution

- Alternative IAM distribution (online B2C web shops, DIY stores, rack jobbers)

- Workshops by target groups (mechanics, tires, check / paint etc.)

- Workshop systems

- Company profiles

- National and international cooperation

- Parts Wholesale (IAM / OES)

- Fast Fitters, car center, online shops, Mass Merchandisersetc.)

Get more information about the Car Aftermarket Europe Report here:

{kind=link}