Skip to content

Skip to content

Chinese Car Brands in Europe: Trends, Challenges, and Future Outlook

Presented by Antti Wolk at AMR 2025, Beijing

On March 31, 2025, Antti Wolk, Managing Director of Wolk & Nikolic After Sales Intelligence, delivered a keynote at the AMR Aftermarket Conference in Beijing. The presentation explored how Chinese car brands are entering the European market, the challenges they face, and how the second wave is reshaping their strategy.

Chinese Car Brands in Europe: Current Market Share

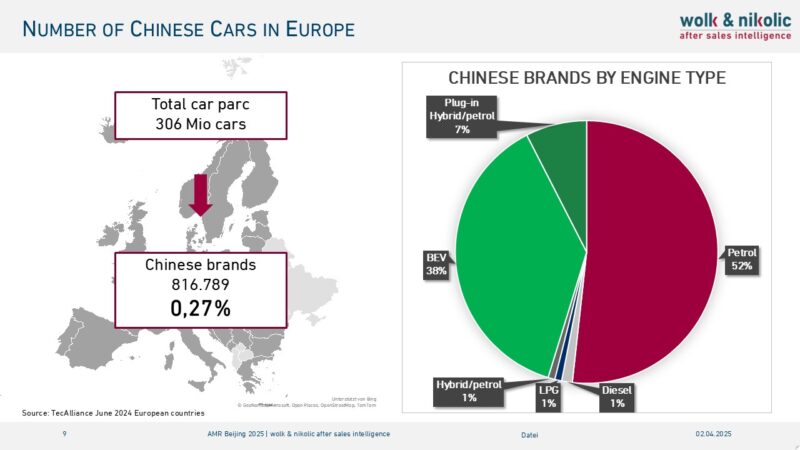

Despite the growing demand for BEVs (Battery Electric Vehicles) in Europe, the overall market share of Chinese vehicles remains modest. As of mid-2024, only 0.27% of vehicles in operation across Europe are Chinese brands—equating to around 816,789 vehicles out of 306 million.

Surprisingly, only half of these Chinese vehicles are electric. The dominance of MG, which still sells a large number of petrol vehicles, accounts for 80% of the total Chinese car presence. Polestar and Lynk & Co follow, while newer EV-focused brands like BYD, NIO, and XPeng lag behind.

2025 Trends: Signs of Change

February 2025 showed a potential turning point. New BEV registrations increased by 16%, and Chinese brand sales grew by 46% compared to the previous year. While overall car sales fell by 2.5%, this growth signals increased interest in electric and Chinese vehicles.

Notably, Volkswagen surpassed Tesla as the top BEV manufacturer in Europe for the first time. Tesla’s decline—down 44%—was largely attributed to Elon Musk’s political controversies.

Why the First Wave of Chinese Cars Struggled

Many Chinese brands followed Tesla’s direct-to-consumer online sales model. However, they lacked the brand awareness and customer trust needed for such an approach. Unlike Tesla, these newcomers did not benefit from a strong public image or established reputation.

The few exceptions—MG, Polestar, and Lynk & Co—succeeded thanks to their heritage and dealer networks. Brands like BYD initially relied on large importers but are now switching to smaller, localized partnerships. Meanwhile, NIO and XPeng are moving toward traditional dealerships.

Is Pricing a Competitive Advantage?

Consumers expect Chinese EVs to be significantly cheaper. While prices are lower than European models, the difference often isn’t enough to drive a purchase decision. Furthermore, equipment levels and digital features have not always met expectations—especially in early MG and BYD models.

The second wave of imports is expected to correct these shortcomings, offering full-featured, tech-savvy vehicles with better pricing propositions.

Marketing Mistakes: Lessons from BYD

Marketing has been another weak point. For example, during the 2024 European Football Championship, BYD’s slogan “No.1 NEV Maker” failed to resonate. Most spectators didn’t understand the brand, its pronunciation, or its connection to electric vehicles as NEV (New energy vehicle) is not such a common abbreviation on the European market.

The takeaway? Localization and customer education are essential. European consumers need to see, touch, and test cars before committing—especially with new brands.

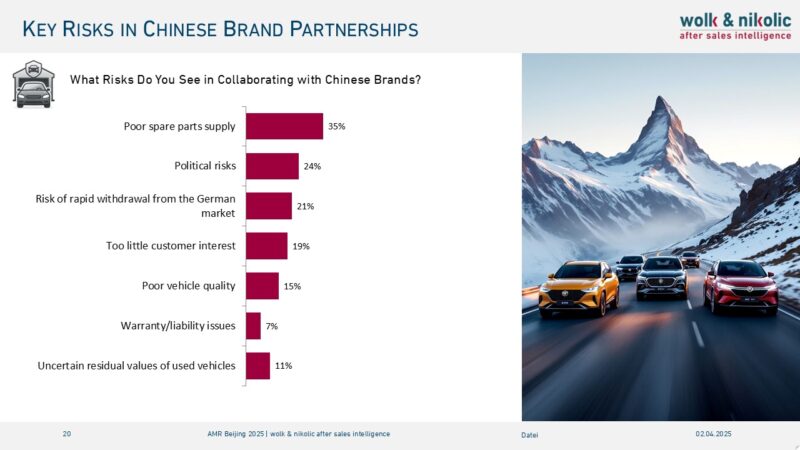

Survey Results: Market Perception in Germany

- Only 25% of workshops and dealers are willing to partner with Chinese brands (down from 38% in 2023).

- 27% of drivers are open to buying a Chinese car—primarily due to good value for money and full-featured tech.

- Concerns include China’s political stance and a potential poor parts supply.

BEV Adoption Still Limited

When asked about their preferred powertrain, only 10% chose full electric and 12% plugin hybrid. Even if only EVs were available, just 4% of respondents would choose BYD. This suggests that Chinese brands face fierce competition from established European manufacturers.

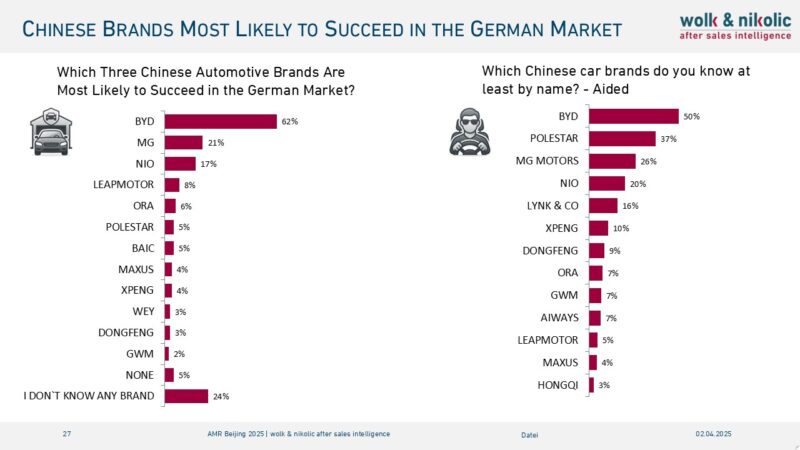

Long-Term Outlook: Second Wave and Beyond

Despite early missteps, optimism remains. Around 70% of car dealers and 61% of drivers believe Chinese brands will succeed in Europe long-term. Among them, BYD is seen as the most promising player, thanks to its scale, momentum, and growing awareness.

The next wave of Chinese automakers will need to focus on:

- Expanding dealer networks

- Improving brand trust and visibility

- Delivering true value through pricing and technology

- Investing in local marketing and customer engagement

Europe’s automotive market is evolving. Chinese car manufacturers must now adapt to its complexity—or risk repeating the failures of the first wave.

Author: Antti Wolk, Managing Director at Wolk & Nikolic After Sales Intelligence

Contact: antti.wolk@wolk-aftersales.de